The Kenyan shilling has repeatedly plunged to record lows this year, weighed down by high oil prices and hard currency demand from sectors, including energy and manufacturing, outmatching supply.

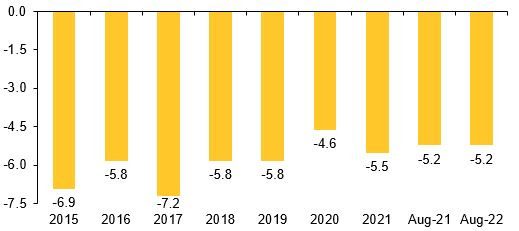

Further compounding pressure on the shilling has been a persistent current account deficit. Provisional data from the Central Bank of Kenya showed that the current account deficit was estimated at 5.2 percent of GDP in the 12 months to August 2022, a similar position to that recorded in the corresponding month of 2021.

According to the CBK, the deficit was supported by receipts from service exports and resilient remittances. Kenya continues to run current account deficits, and this could see the shilling, which remains overvalued on a real effective exchange rate basis, extend its bearish run in the near term. Looking to this week, dollar demand from fuel importers and corporate clients is set to outweigh supply, suggesting that the selling pressure is unlikely to abate.

{kind=link}