We will consider a feasible framework (Botswana context) reflecting governance relationships that may exist for a local institutional fiduciary firm which we will call, for purposes of this article, the Botswana Peoples’ Pension Fund. (BPPF), we shall also look at the particular roles that each member of the governance relationship framework plays, as well as how their activities feed into the functions of other framework constituents.

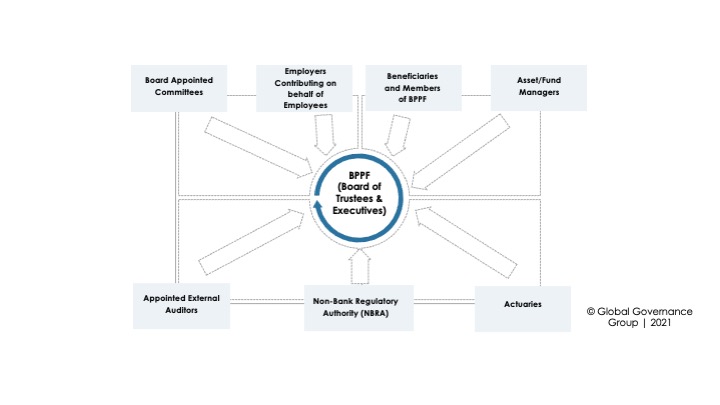

The governance relationship framework, as shown in the diagram, comprises a number of parties crucial for the effective governance and consequently, smooth functioning of the Botswana Peoples’ Pension Fund as it pursues its fiduciary mandate. The pension fund’s mandate would ordinarily entail administration of member contributions, determination of member benefit eligibility, and asset management solutions to meet beneficiary needs, whilst it simultaneously adheres to set standards and legislation.

A pivotal party highlighted in the framework is the regulator, which in this case, we have termed the Non-Bank Regulatory Authority (NBRA). Closely linked to the responsibility for adherence to legislation mentioned above, the NBRA is empowered by the state with oversight functions of scheme regulation, development of practice provisions and codes, operative guidance and amendment of laws affecting the BPPF as a going concern. To the extent that the BPPF is a statutory establishment, there may also be a particular legislative instrument underpinning its regulation concurrently with NBRA statutes.

From the perspective of accountability on the financial front (considering that the BPPF is a steward of funds contributed by firms and individuals), the external auditor appointed by the Board is another crucial player in this framework, which has the task of ensuring appropriate internal adherence to accounting standards and accurate integrated reporting to enable other members of the relationship framework such as beneficiaries and the regulator to have an understanding of the internal management and administration of finances within the organization. Informed judgements can then be made regarding the BPPF’s financial conduct, soundness and standing on this basis.

The roles of the actuary and asset manager in the governance relationship regime are quite closely intertwined. The BPPF should ensure that it is in a position to pay the requisite fees for indispensable investment insight and actuarial advice such that beneficiaries’ chances of meeting their varied investment objectives through the BPPF are increased to a substantial extent. Asset managers have the essential research capacity, market knowledge and investment prowess to assist on this journey of safeguarding beneficiary interests, whilst the actuaries are best positioned to assist with respect to engagement with lawyers and other crucial administrators for achievement of set objectives.

A significant proportion of the funds poured into pension funds are from varied employers providing defined-benefit and/or defined-contribution alternatives for their employees. From the perspective of the magnitude of monetary sums that they bring in, they play a major role in the governance relationship framework. With the increasing sophistication of pension funds in terms of their offerings to firms and individuals as well as technology and ease of access to the solutions that they offer, the beneficiaries and members constituency of the governance relationship framework would comprise individuals investing in their personal capacity, for example, small business owners with long-term family interests that they wish to safeguard.

In previous articles relating to Board inductions and evaluations, we have highlighted the responsibility of Boards of Directors (trustees in the case of the BPPF) appointing committees as they undertake their governance and accountability duties. These committees are crucial constituents of the governance relationship framework as they oversee a wide range of important aspects as decided upon by the BPPF Board, including internal audit, finance and procurement, research and development, compensation, investigations (where internal misconduct may be identified), as well as disciplinary considerations as the organization operates.

It is consequently important to bear in mind that the existence of such frameworks that outline governance relationships is overly crucial for avoidance of fiduciary duty breaches. Establishment of organizational governance relationships, and a solid understanding thereof, can go a long way in curtailing cases where parties within the framework such as Boards, asset managers and employers may act at the expense of other parties within the governance relationship mechanism, which in many instances tends to be the beneficiaries.

The views and opinions expressed in this article are those of the author, Dumisani F. Ntini – Governance and Strategy Practitioner.

Contact info@governancegroup.org. Visit www.governancegroup.org.

LinkedIn: Dumisani F. Ntini

Facebook: BigBudget

YouTube: BigBudget

Instagram: biggbudget

{kind=link}